March 2026

- James Kim

- Apr 7

- 8 min read

North America

·RXR scrambles to save the 230 Park Avenue as CMBS clock ticks. RXR has secured a one-month forbearance extension on its $670m CMBS loan against the Helmsley Building at 230 Park Avenue, buying the landlord additional time to restructure ahead of what would otherwise be a foreclosure process. The loan, which matured in December 2023 and transferred to special servicing two months prior, has seen total exposure creep to $699.7m as tax, insurance and interest advances accumulate. Occupancy stood at just 55.8% as of the September rent roll, and S&P Global has cut its net recovery value to $368m, some 52.8% below the July appraised value of $780m, implying deep impairment for bondholders in a recovery scenario. The paradox is striking: the building simultaneously posted its highest-ever asking rent in February, with StoneX expanding into a 10-year, $120/sq ft deal, a data point that speaks to the barbell nature of the post-pandemic office market, where headline rents and occupancy can diverge sharply. Lenders and special servicers across the market are watching the loan resolution closely, as the Helmsley represents a bellwether for a broader wave of maturing office CMBS loans in 2026. For distressed investors, the gap between S&P's $368m recovery estimate and the loan balance offers a potential entry point, though the capital expenditure required to stabilise occupancy will weigh heavily on underwriting. (Source: CoStar, Green Loan Services, S&P Global, 2026)

Lenders are looking to foreclose on Helmsley Building, 230 Park Avenue, New York

·Demolitions and conversions push US office stock into decline. The U.S. office market has effectively stopped growing, as rising demolitions and conversions offset limited new construction. CoStar data show quarterly office starts holding near record lows of around 5 million square feet, the weakest since 2011. Meanwhile, the pace of removals has surged, with quarterly demolitions jumping to nearly 10 million square feet by late 2025. A more stable rate environment and improved valuations since 2024 have reignited redevelopment activity, turning many obsolete offices into housing or hotels. The volume of space suitable for conversion (older, smaller, high-vacancy buildings) has climbed 40% since mid-2023 to 112 million square feet. Vacancy remains highly concentrated in underperforming assets, which are increasingly exiting the office inventory altogether. While these removals won’t lift rents directly, they mark a crucial structural reset that should stabilise vacancies and revitalise urban markets. (Source: CoStar, 2026)

Office Construction/ Supply Growth Trend

·US hotels open strong in 2026, but geopolitics cap the upside. The US hotel sector has begun 2026 on firm footing, with RevPAR growth through mid‑March running in the low‑single digits and improving on a four‑week moving‑average basis. Strength is broad‑based by segment and geography, reflecting resilient travel demand despite last year’s tariff shock. Comparables turn meaningfully easier from April as the industry laps nine consecutive months of tariff‑driven RevPAR declines, setting up supportive optics for the rest of the first half. Corporate travel budgets and policies now largely embed the tariff regime, while TSA data continue to signal solid air travel from higher‑income cohorts. Mid‑June to mid‑July World Cup fixtures are expected to add a demand and pricing kicker in the 11 host cities, especially in later‑round matches. However, the war in Iran and the associated spike in oil prices present a clear downside risk via higher airfares, gasoline and potential second‑round inflation effects. CoStar’s base case still calls for just 0.6% RevPAR growth in 2026, as favourable comps and event‑driven upside are broadly offset by energy‑related demand headwinds.

US RevPAR Percentage Change (4 week average)

·Sun Life Financial’s BentallGreenOak acquires Bell Partners in $350m deal to build US multifamily platform. Sun Life Financial (Toronto-listed insurance and asset management group) has agreed to acquire 100% of Bell Partners, the Greensboro-headquartered multifamily investment manager, for $350m with closing expected in H2 2026. Bell Partners manages approximately 70,000 apartment homes across 12 US regions, with $10bn in assets under management spanning markets from Seattle to Boston. The acquisition sits within Sun Life's BentallGreenOak (BGO) real estate unit, which Sun Life simultaneously fully consolidated by buying out the remaining 44% it did not already own for $1.59bn, signalling a decisive push to build institutional-scale real estate capability. Combined, BGO and Bell Partners will oversee more than $100bn of real estate AUM globally, positioning the platform among the largest US multifamily investment managers. The vertical integration of Bell's property management capability is the strategic prize: it gives BGO in-house operational infrastructure that pure capital allocators typically lack and which underpins both performance and fee diversification. The deal comes at a nuanced point in the US apartment cycle. CoStar projects net deliveries to marginally exceed absorption through 2026, keeping vacancy elevated near-term. Sun Life's all-in commitment suggests conviction in the medium-term supply correction thesis. (Source: Sun Life, BentallGreenOak, Bell Partners, CoStar, 2026)

Bell Partners’ Block Loft Apartments in Old Fourth Ward, Atlanta

·Hines pivots to fundamentals-driven strategy with $1bn+ deployed across living, industrial and alternatives. Hines, the Houston-based global real estate investment manager with a ~$92bn portfolio, has deployed more than $1bn over the past 18 months into what it terms fundamentals-driven acquisitions including data centres, self-storage and residential assets in supply-constrained, high-growth markets as geopolitical and economic volatility reshapes its underwriting priorities. Recent deals include a fully leased San Diego-area data centre, multifamily assets in Los Angeles exurbs and self-storage facilities in Nashville and Chicago, with the firm's primary vehicle, Hines US Property Partners, now valued at more than $3.5bn. The strategic shift marks a deliberate retreat from broad-based opportunistic dealmaking toward assets where demand is underpinned by population growth, digital infrastructure requirements or geographic supply barriers rather than sentiment. Office is no longer a uniform allocation for Hines, with capital directed selectively toward trophy assets capable of commanding hospitality-grade amenities, a thesis validated by renewed leasing momentum at 101 California Street in San Francisco and 1125 17th Street in Denver, and by JPMorgan Chase anchoring roughly 65% of the office component at the recently completed $1.5bn South Station Tower in Boston. The broader message from global co-head of investment management Alfonso Munk is one of deliberate capital selectivity: conservative underwriting, proximity to local operating teams and a preference for long-duration income drivers over near-term multiple expansion. (Source: CoStar, Hines, 2026)

Hines acquires self storage facility in Chicago, US

Europe

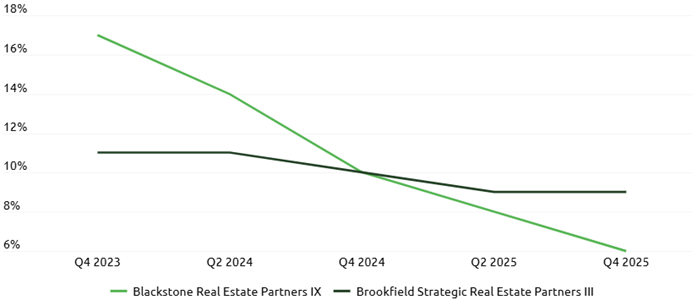

·Pre-Covid private equity vintage funds lag: $45bn of unrealised assets and dwindling time. The largest global and European private equity real estate funds raised in 2018 and 2019, including vehicles from Blackstone, Brookfield, TPG, Ares and Angelo Gordon, collectively hold more than $45bn in unrealised investments, having exited just over $30bn to date, underscoring the scale of the industry's disposal challenge. Persistently elevated interest rates have suppressed exit pricing and incentivised managers to hold. Across the cohort, reported net IRRs have broadly trended downward, with vintage and geography proving material differentiators. Cambridge Associates data shows 2018 global opportunistic funds delivering median net IRRs of 8.9% versus just 5.5% for 2019 vintage equivalents. TPG stands out as the notable outperformer, with TREP III reporting an 11% net IRR, up from 9% two years ago, driven by data centre holdings and appreciation across hotel, residential and office portfolios, and is the most advanced on realisations with only $2.4bn remaining. Blackstone's flagship vehicles tell a more cautionary tale, with BREP IX's IRR falling from a peak of 34% in Q3 2022 to 6% today as logistics yield expansion unwound post-Covid gains, though the firm still holds $25bn-plus in unrealised value across its global and European funds. Brookfield and Ares are broadly in line with European peers at 9% and 3.6% net IRR respectively, while both firms' US vehicles continue to outperform their European equivalents by a meaningful margin. (Source: Green Street, Cambridge Associates, Blackstone, Brookfield, TPG, Ares, Angelo Gordon, 2026)

Private Equity Fund Performance- 2018 and 2019 Vintages

Fund Net IRR Performance Trend (BREP IX v. BSREP III)

·Savills agrees blockbuster £900m acquisition of Estadil Secured. Savills has agreed to acquire Eastdil Secured, the preeminent global real estate investment bank, for an enterprise value of approximately £900m (c. $1.1bn), in one of the most significant deals in the firm's history. The deal provides an exit for Guggenheim and Temasek, who acquired Eastdil from Wells Fargo for $400m in 2019 following a management-led recapitalisation. For Savills, the acquisition delivers an immediate, scaled presence in the US capital markets alongside top-tier equity and debt advisory capabilities that are largely absent from its existing platform. The combined group will rank as the number two advisory firm globally for prime commercial real estate transactions above $100m, based on MSCI data for 2021–2025. Eastdil will continue to operate as the Group's dedicated real estate investment bank, retaining its brand, culture and day-to-day independence. The deal marks a consequential opening move for Savills' incoming CEO Simon Shaw, signalling that the firm is positioning itself at the apex of institutional real estate advisory on both sides of the Atlantic. (Source: Savills UK, Green Street, Yahoo Finance, 2026)

·Bundesbank HQ search puts Frankfurt office market in play. Germany's Bundesbank has abandoned plans to refurbish its existing 10-hectare Bockenheim campus, costed at €1.6bn and instead announced it will forward purchase a new Frankfurt HQ of at least 50,000 sq m with capacity for 3,300 workplaces, with a decision expected within 18 months. The central bank has ruled out leasing and will not act as developer, with the acquisition to be conducted via public tender, creating a rare and sizeable occupier-driven demand event in one of Europe's most challenged office markets. Patrizia has moved quickly to position the 78,000 sq m Eurotower, managed on behalf of Taiwanese insurer Fubon Life since a €530m acquisition in 2018, as a leading candidate. Competing assets include Art-Invest's Trianon, where any deal is contingent on Bundesbank committing to the full 68,000 sq m, Invesco's Die Welle at a €400m asking price, and new developments such as Tishman Speyer and Commerz Real's Gloria tower, targeting 2030 completion at 60,300 sq m. Patrizia is simultaneously exploring refurbishment strategies for Eurotower ranging from light touch to full redevelopment, with potential mixed-use conversion including hotel, though any forward deal would require material capital commitment from Fubon Life. (Source: Green Street, Bundesbank, Patrizia, 2026)

Eurotower at Willy-Brandt-Platz in Frankfurt

·Indonesian investor returns to London offices with £140m Burberry HQ acquisition. Derwent London has agreed to sell Horseferry House in Westminster, Burberry's global headquarters, to Indonesian developer Sinar Mas Land for approximately £140m, reflecting a yield of circa 6.2%. The Jakarta-based buyer, the largest developer of its kind in Indonesia, is making a return to the London office market having last transacted here in 2022 when it acquired 40 Strand from Landsec for £195m. The 160,000 sq ft building generates passing rent of around £8m per annum, with Derwent having extended Burberry's lease to 2043 ahead of the sale and incorporated two new five-yearly fixed uplifts, providing the incoming investor with circa 17 years of secure, escalating income. Horseferry House sits in Victoria rather than on prime West End pitch, and the 6.2% yield reflects that location differential relative to core Mayfair or St James's assets, where long-let trophy offices have traded meaningfully tighter. Sinar Mas has demonstrated consistent appetite for long-income London offices, with prior acquisitions including Alphabeta Building and 33 Horseferry Road, the latter acquired for £188.6m and subsequently sold for £247.5m, and the transaction follows a near-miss on 20 Old Bailey in early 2024. (Source: Green Street, Derwent, Sinar Mas Land, 2026)

Horseferry House situated in Westminster, London

·UBS suspends redemptions on €400m+ Euroinvest Immobilien fund for up to 36 months. UBS Real Estate GmbH has suspended redemptions and share issuance on its open-ended UBS Euroinvest Immobilien fund for up to 36 months, citing the geopolitical and economic environment stemming from the Middle East conflict and escalating energy prices. The €400m+ vehicle, launched in 2019, targets core real estate across European cities. The suspension marks the first major European real estate open-ended fund closure since the outbreak of hostilities in the Middle East, underscoring the structural vulnerability of daily-dealing vehicles to sentiment-driven redemption spikes. The trigger, a sharp increase in withdrawal requests threatening liquidity for remaining investors, reflects the classic first-mover disadvantage that open-ended fund structures carry in risk-off environments. The dynamic is not isolated to real estate: Apollo, Ares, and BlackRock have all imposed restrictions on withdrawals from major US private credit vehicles in recent weeks as macro anxiety mounts. In Germany specifically, Wertgrund and Industria Immobilien had already closed their open-ended residential funds earlier this year citing insufficient liquid assets, suggesting the sector was already under strain ahead of the UBS move. For institutional investors, the episode reinforces long-running questions around the liquidity mismatch inherent in open-ended structures and whether current pricing adequately reflects the redemption risk premium. (Source: Green Street, UBS, Apollo, Ares, 2026)

Comments